We take a look at how COVID-19 is having an impact on the economy and the property market and pull together what the experts think will happen once the pandemic calms down.

Economy

Interest rates were cut to just 0.1% in mid-March their lowest ever level, with some economists predicting Coronavirus will create a short, sharp v-shaped economic impact on the UK. Oxford Economics predicts rates will remain at this level until the autumn of 2021. UK inflation was 1.7% in February, down from 1.8% in January and below the government's 2% target.

According to HM Treasury latest consensus forecasts for GDP growth (made between 1st and 14th April) are -5.8% for 2020 and 5% for 2021. The current shutdown will have the biggest impact on the second quarter with the economy expected to shrink by -12.2%.

Levels of confidence have a significant bearing on the housing market. Understandably in the current situation, confidence in personal finances and the wider economy have taken a hit with the GFK consumer confidence reporting the most significant fall since records began in 1974 and the largest since the 2008 global financial crisis. Meanwhile, the RICS Residential Survey also reported house buyer sentiment deteriorating sharply in March.

Prices

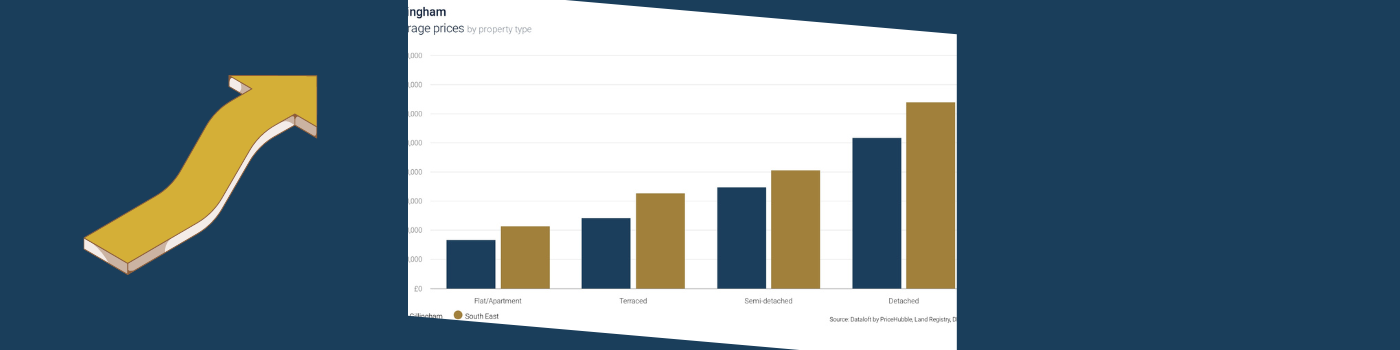

The average price of a property sold in the UK in February was £230,332, 1.1% higher than a year ago, according to the latest data from the UK House Price Index. Wales saw the largest annual increase, 3.4%, and the East was the only region to see a decline, -1%. Within the Medway market prices have dropped slightly on the year with the average house price at £249,620 which is a decline of -0.74%

It will be difficult to gauge the impact of coronavirus on house prices in the short term due to the near stall of transactions but it appears that many homeowners are still requesting valuations of their property according to the on-line Val-Pal network which states they are seeing close to 1,000 requests a day.

RICS Residential Survey reported near term price expectations sinking from a net balance of +21% in February to -82% in March. The 12-month view is less negative with a net balance of -38% and the 5-year outlook is virtually unchanged averaging +2.5% per annum.

Transactions

Seasonally adjusted it is estimated 99,440 sales took place in March, up 0.3% on a year ago, showing a reflection of the market pre-COVID. This is however likely to be revised downwards. Sales levels for February have been revised downwards by 4.1% to 99,650, 1.1% higher than February 2019. The market in Medway paints a slightly different picture with transactions down to 255 in January 2020 compared with 306 in January 2019.

Zoopla reports the number of agreed property sales fell by 70% in the first two weeks of lockdown. Restrictions on moving into new homes are delaying completion dates although a Dataloft agent survey suggests that the majority of buyers who committed to deals before lockdown are still progressing with the conveyancing process and not withdrawing from purchases.

Although some agents are still reporting sales agreed, few transactions are likely to register in the next few months. Savills predict sales volumes may fall between 20%-40% of the five-year average by June with Knight Frank estimating there will be 734,000 sales this year, 440,000 fewer than in 2019.

Demand

In the run-up to the COVID-19 crisis, demand levels had been building in the market. 73,456 mortgages were approved in February, the highest monthly total since January 2014 at the peak of the housing market, even exceeding approvals in the run-up to the 3% stamp duty surcharge. With the Coronavirus pandemic pausing activity at present, it remains to be seen whether and how quickly this pent up demand releases once lockdown is lifted.

There has been no mass exodus of properties from the market following the Coronavirus lockdown. Zoopla report stock levels per agent on 7th April were only 1% lower than 7th March. Rightmove reports that available stock for sale is only down 2.6% since lockdown. This tallies with the recent Dataloft survey where 81% of agents reported the majority of vendors were keeping their properties on the market.

Demand levels are difficult to measure at the moment with in-person viewings of properties impossible and deals unlikely to be agreed. Understandably the RICS and Zoopla are reporting fewer buyer enquiries. There is some evidence though that potential buyers are still browsing for new homes. Both Rightmove and Zoopla are reporting some increase in online property searches after an initial drop-in visits in the initial period of lockdown.

Investment/lettings

Average rental values across the UK rose by 1.4% in the year to March, unchanged since February 2020 (IPHRP), the highest annual growth currently in the South West and East Midlands. The buy to let market in Medway over the last 12 months has been performing very well with a 5% increase on the previous 12 months, with the average rent is £825 per month. Which is higher the South East average of 2.7%

However, RICS Residential Survey reports Coronavirus having a negative impact on near term rental growth, with rents stagnating over the next 12 months. Fortunately, the 5-year forecast remains positive with an average annual growth of 2.5%.

From 1st April 2020, all rented properties must hold an EPC rating of E. Landlords of properties below this rating with existing tenants are obliged to carry out works worth up to £3,500 to improve their energy efficiency. If an upgrade to EPC E cannot be achieved within this limit landlords are required to register for an ‘all improvements made’ exemption.

Development/new build

Just under 145,000 new private homes were completed in 2019, the highest annual total since 2007, according to data released by the government. Completions were up 7.6% year on year. In comparison, the number of private new homes started fell 10% to 124,250, its lowest total since 2015. The cessation of construction due to Coronavirus will impact the ability of planning authorities to reach housing targets. The total value of new build transactions over the last 3 months £32.8M within the Medway market.

As yet COVID-19 has had little impact on the number of the planning pipeline according to Barbour ABI and planning decisions are still being determined. Under the Coronavirus Act 2020, the government has made a temporary amendment to the law to allow planning meetings to be held via video link until 31st May 2021.

There have been rumours that Help to Buy could be extended in an attempt to kickstart the housebuilding industry after lockdown is lifted.

Prime markets

Many agents are revising their prospects for the market as a result of COVID-19. Savills predict 5-year growth across PCL will remain at 20% although acknowledge yearly growth will differ from their original forecasts. Knight Frank report that the annual decline in PCL sales was only down 1.1% in March due to a strong start to the year, they believe strong prices will remain unchanged in 2020 as PCL has already seen declines of around 20% since 2014. PCL will recover sharply in 2021 with an 8% growth.

Ahead of COVID-19 London retained its second place behind New York in the latest edition of the Global Financial Centres Index. With the exception of San Francisco (ranked 8th), nine of the top 10 cities saw their rating score fall. The ranking is an aggregate of indices from five key areas: business environment, financial sector development, infrastructure factors, human capital and reputation, and general factors.

From April 2021 non-UK residents will face an additional 2% Stamp Duty Land Tax levy on residential property purchases in England and Northern Ireland. However, the weakness of the pound will continue to drive demand, according to Knight Frank discounts of more than 30% are available for a range of overseas currencies compared to mid-2014.

By

By

Share this with

Email

Facebook

Messenger

Twitter

Pinterest

LinkedIn

Copy this link